“We believe that by focusing on making payments more accessible, efficient, and secure, UPCX will lead the way in the future of finance. UPCX’s vision is not only to create a better blockchain but to create new opportunities by providing individuals and businesses with the tools they need to take their financial future into their own hands.” – UPCX Whitepaper.

The Importance of Financial Inclusion

Financial inclusion is a crucial strategy for ensuring that all segments of society, particularly low-income and vulnerable groups, have access to and can afford appropriate financial products and services. This encompasses not only essential banking services like opening bank accounts and saving but also credit, insurance, and payment services. Through these services, individuals can better manage their finances, enhance their resilience to financial crises, support entrepreneurial activities, invest in education, and contribute to overall economic growth.

The Persistent Gap in Financial Inclusion

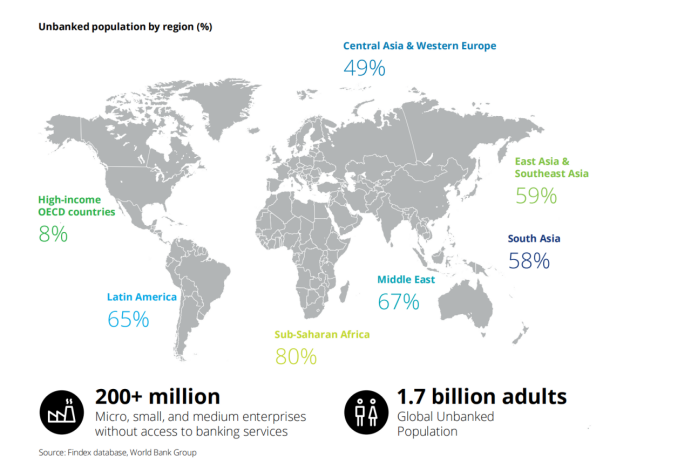

Despite progress in financial inclusion globally, a significant gap remains. Data shows that 94% of adults in high-income countries have bank accounts, compared to only 63% in low and middle-income countries. Approximately 1.7 billion people worldwide remain unbanked, with the majority residing in Africa, Asia, Latin America, and the Middle East, often living on less than $2 a day.

Furthermore, over 200 million micro, small, and medium-sized enterprises (MSMEs) in emerging markets face challenges accessing traditional banking services. These enterprises play a crucial role in employment and GDP contribution but encounter numerous barriers to accessing financial services.

Factors Contributing to Financial Service Inequality

Several factors contribute to this inequality in access to financial services:

- Geographical Barriers:Limited or inconveniently located branches of financial institutions.

- Economic Barriers:Costs associated with financial services are too high for low-income groups.

- Identification Barriers:Lack of necessary personal identification documents.

- Household Factors:Existing family members with bank accounts reduce the need for individual accounts within the household.

- Religious Factors:Religious beliefs restrict the use of certain financial services.

- Lack of Trust:Distrust in financial institutions.

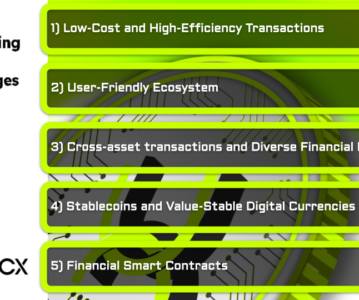

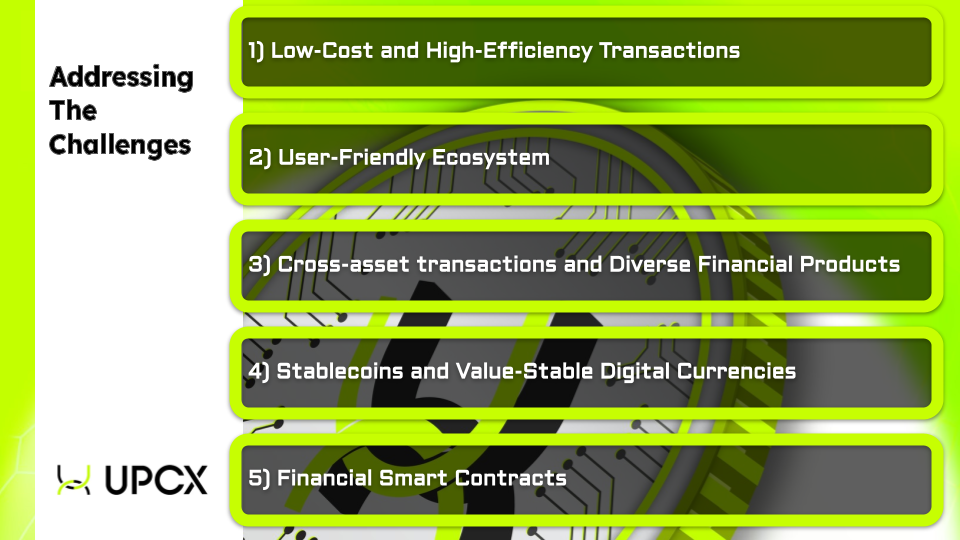

Addressing the Challenges: Blockchain and UPCX

To address these challenges, new financial technologies and business models, such as blockchain technology, offer promising possibilities. In particular, the innovative blockchain payment system UPCX has the potential to enhance financial inclusion through various means significantly:

1) Low-Cost and High-Efficiency Transactions

UPCX leverages its Graphene-based blockchain system to significantly improve transaction efficiency, processing millions of transactions per second and achieving a settlement within 1 second. The platform utilizes sharding technology, dividing the blockchain into multiple sub-chains for parallel processing, thereby increasing throughput and reducing costs. Additionally, by removing traditional financial intermediaries like banks and clearinghouses, transactions occur directly between buyers and sellers, enhancing transparency and enabling near real-time transaction completion.

These technological advantages are particularly well-suited for low-income users and MSMEs who require frequent, small-value transactions, providing them with a low-cost and efficient solution. Therefore, UPCX’s blockchain payment system not only possesses significant competitiveness in the global financial market but is also especially suitable for users and businesses seeking reliable and cost-effective payment services.

2) User-Friendly Ecosystem

UPCX significantly lowers the technical barrier by providing user-friendly development tools and APIs, enabling developers to create and deploy blockchain-based applications easily. This openness and flexibility empower innovators and entrepreneurs to develop customized solutions that meet specific needs. For example, small businesses can rapidly develop payment systems without deeply understanding the underlying blockchain technology.

Furthermore, UPCX utilizes blockchain technology to simplify the account opening process. Users can authenticate with simple biometric information through a blockchain-based digital identity system, eliminating the need for cumbersome documentation and verification procedures. This facilitates online and mobile payments, which is particularly beneficial for low-income and vulnerable groups. These features collectively create a user-friendly blockchain ecosystem that increases the accessibility and adoption of the technology.

3) Cross-asset transactions and Diverse Financial Products

Promoting financial diversification, UPCX supports transactions across various asset classes, including cryptocurrencies, fiat currencies, and other digital assets. This platform offers a one-stop financial solution, helping not only various financial products such as debt, equity, and insurance but also microloans, microinsurance, and microsavings products designed for low-income individuals. These products emphasize low amounts and high flexibility, utilizing smart contracts for automated management and distribution, aiming to reduce service costs and make financial services more affordable and accessible.

Moreover, the UPCX platform provides fast and low-cost cross-border payment and remittance services, which are particularly suitable for low-income families reliant on remittances from abroad. By utilizing stablecoins or other digital currencies, the platform can significantly reduce the cost and processing time associated with traditional remittance methods. Overall, the UPCX platform, by integrating various assets and financial services, dramatically increases the flexibility and convenience of transactions while offering solutions that effectively support low-income groups.

4) Stablecoins and Value-Stable Digital Currencies

To mitigate risk, the UPCX platform supports the issuance of stablecoins pegged to the price of real-world assets such as fiat currencies and commodities, utilizing highly reliable price oracles to ensure price accuracy. This stablecoin mechanism not only allows users to process and complete transactions involving real-world assets within the UPCX platform but also provides users with a value-stable method for payments and value storage. For users experiencing high volatility in their national currency, stablecoins are particularly significant as they offer an effective way to avoid currency price fluctuations and devaluation. Stablecoins can be used for both daily transactions and as a tool to combat economic instability.

5) Financial Smart Contracts

Addressing the trust crisis, the UPCX platform utilizes financial smart contracts to automate the execution of complex financial services such as loan disbursement, insurance claims, and debt settlement. These smart contracts enhance processing speed and transparency by reducing human intervention and potential fraudulent activities. Once encoded into the blockchain, the contract terms become immutable, strengthening the security and trustworthiness of transactions.

6) Conclusion

While the UPCX platform offers potential solutions to promote financial inclusion, achieving this goal requires a coordinated effort with appropriate regulatory frameworks and continuous technological innovation. Additionally, financial education and enhancing financial literacy are crucial steps, especially for low-income and vulnerable groups. Through mobile applications, online courses, or interactive educational modules within the trading platform, basic financial knowledge and digital financial tools can be effectively imparted to these groups. Only by integrating these measures can we eliminate barriers to the accessibility and affordability of financial services, thereby achieving global financial inclusion.

In conclusion, the UPCX platform provides powerful tools and solutions to enhance global financial inclusion through its innovative blockchain technology and diverse financial products. Through low-cost transactions, a user-friendly technology platform, and cross-asset and cross-border flexibility, it can effectively serve low-income and vulnerable groups often overlooked by the traditional financial system.

Furthermore, the introduction of stablecoins and the application of smart contracts further strengthen its ability to combat economic instability, providing users with safer and more convenient financial services. With the development and application of these technologies, we anticipate a more equitable and inclusive financial future where everyone can access and utilize adequate financial resources, thereby improving their quality of life and economic well-being.